?unique=6d83875)

The Corporate Sustainability Reporting Directive (CSRD) introduces new requirements for companies regarding the disclosure of sustainability information. While this may seem challenging for many organizations, with the right approach, CSRD compliance can be smoothly integrated.

In this blog, we outline the initial requirements for CSRD compliance and share practical tips and best practices. Using Ørsted as an example, we demonstrate how you can optimize your sustainability reporting and create value for both your organization and its stakeholders.

Step 1: Identify and Categorize Stakeholders

Stakeholders include any individuals or groups that are directly or indirectly affected by your business activities. This may include employees, customers, suppliers, investors, NGOs, and even nature itself as a silent stakeholder.

How to proceed:

- List affected stakeholders: These are groups whose interests are impacted by your operations, such as local communities or environmental interests.

- List users of sustainability statements: Think of investors, labor unions, NGOs, and others who rely on your sustainability disclosures.

Tip: Although the European Sustainability Reporting Standards (ESRS) do not formally require you to engage directly with stakeholders, it is advisable to map their interests. This can be done without direct consultation.

Step 2: Stakeholder Engagement – When and How?

While there are no strict requirements for actively involving stakeholders in the reporting process, they can provide valuable insights into which sustainability topics are most relevant for your strategy.

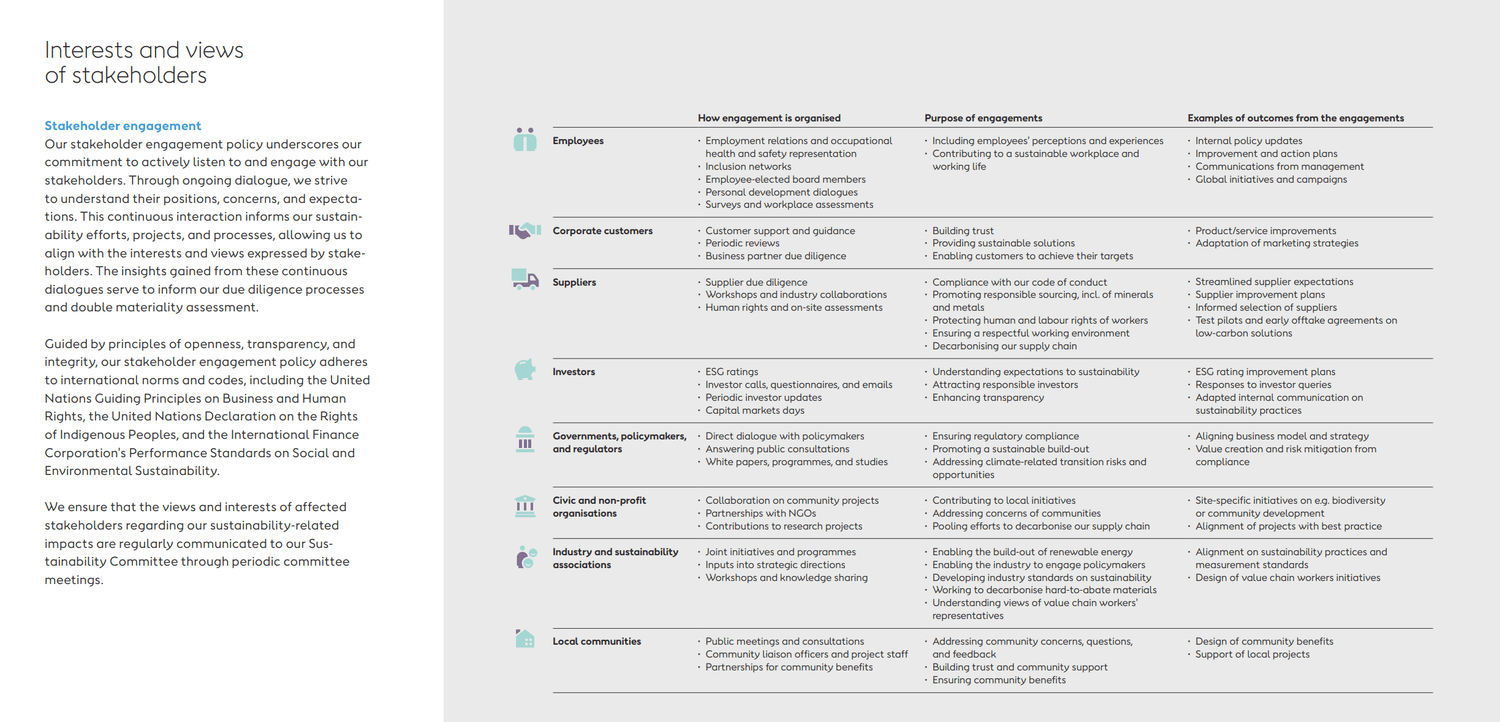

Ørsted Example

Ørsted, a leader in renewable energy, has developed a comprehensive stakeholder overview that clearly outlines the interests and perspectives of its stakeholders. They show how these stakeholders have contributed to their sustainability strategy, though they do not always distinguish between "affected" and "informed" stakeholders — an area where further transparency would benefit CSRD compliance. [Click here for Ørsted’s sustainability report.]

How to proceed:

- Active engagement is optional: You may conduct interviews or surveys to gather insights, but this is not mandatory.

- Accounting Directive obligations: Inform management and employees about the collected sustainability data and how it is gathered and verified.

Tip: Even without direct engagement, you can incorporate stakeholder interests into your materiality assessment. This will help identify key sustainability topics.

Step 3: Conduct a Materiality Assessment

A materiality assessment helps determine which sustainability topics are most relevant for your organization and stakeholders. This is a critical component of CSRD reporting.

How to proceed:

- Collect data on stakeholder interests, even if no direct engagement has taken place.

- Use this data to identify which sustainability topics are “material” and should be included in your report.

Tip: A thorough materiality assessment ensures your sustainability strategy not only complies with CSRD requirements but also adds real value to your organization and its stakeholders.

Step 4: Ongoing Evaluation and Disclosure

The CSRD requires that your sustainability reporting is regularly reviewed and updated to reflect new developments and evolving stakeholder expectations. This ensures your reporting remains current and relevant.

How to proceed:

- Schedule annual reviews of your sustainability strategy to ensure it remains up to date.

Building a Stronger Sustainability Strategy

CSRD compliance may seem complex, but with a structured approach, you can effectively meet key requirements such as materiality assessments and stakeholder engagement. Ørsted demonstrates how transparency around stakeholder engagement can contribute to the success of a sustainability strategy. By clearly identifying which stakeholders are involved and which are informed, you can develop an even stronger and more resilient sustainability policy.